There Is No “Mild” Version of This

Finans.dk wants you to believe the Danish regulator gave Lars Topholm a slap on the wrist. Here is the actual document he produced, the actual chain of events it triggered, and the actual money that w

On 8 April 2026, Finans.dk published its account of the Finanstilsynet decision against Lars Topholm.

The framing was surgical. The reprimand was “den mildeste sanktion” — the mildest sanction. The note had “no price effect.” Topholm’s shares were worth “omkring 130.000 kr.” The case was closed. And then — almost as an afterthought — Finans pivoted to listing Mark Abraham’s lawsuits against Finans itself, Carnegie, Topholm, the board, Nasdaq, the trustee, and Kromann Reumert. The implication: a minor infraction, blown out of proportion by a litigious Romanian CEO.

This framing is a lie of architecture. Every fact Finans quoted is accurate. Every conclusion it guided you toward is false.

Let me show you why. With the actual document. With actual numbers. With actual charts. And with the actual chain of events that took Shape Robotics from a DKK 35 million capital raise to a DKK 1.58 share price — a 97% destruction of value that began with the note Lars Topholm now calls “back of the envelope.”

First: look at the actual document

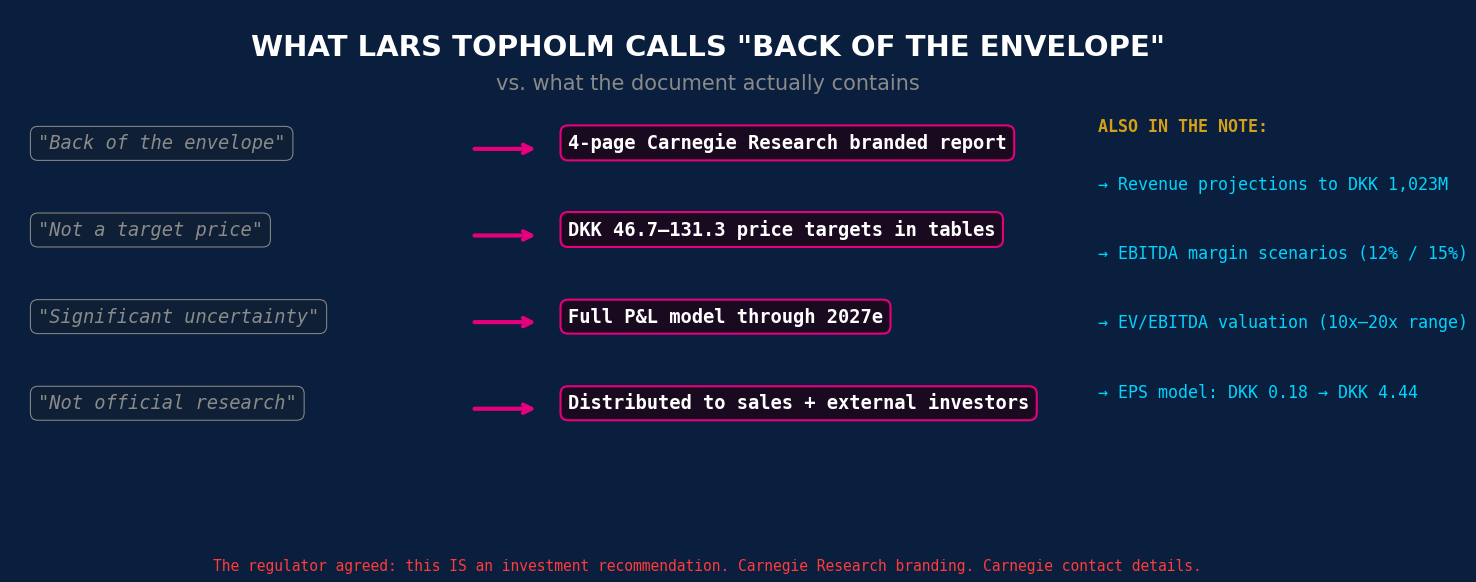

I have the note. Four pages. Let me tell you what it contains.

Topholm calls it “a back-of-the-envelope” analysis. The Finanstilsynet calls it an investment recommendation. Even Finans.dk, in its own article, acknowledges the regulator’s classification. Here is what the document actually contains:

Page 1: A revenue projection chart showing Shape Robotics growing from DKK 171M (2023) to over DKK 1,000M by 2027. Source label at the bottom: “Source: Carnegie Research; company data.” Not “Lars’s personal notes.” Carnegie Research.

Page 2: Two complete valuation tables. The first models a theoretical share price range of DKK 46.7 to DKK 105.1 at a 12% EBITDA margin, using EV/EBITDA multiples of 10x–20x, discounted at an IRR of 15%. The second models DKK 58.4 to DKK 131.3 at a 15% EBITDA margin. These are not scribbles. These are structured DCF-adjacent valuations with explicit assumptions about net debt (NIBD/EBITDA = 2x), share count (14 million), and discount rates.

Page 3: A full projected P&L from 2022 to 2027, including: revenue forecasts to DKK 1,023M, gross margin declining from 28% to 24%, EBITDA margin expanding from 5.9% to 13.9%, EBIT projections, net financials, pre-tax profit, tax at 25%, net profit projections, EPS projections from DKK 0.18 to DKK 4.44, and a PEG ratio calculation suggesting a P/E of 30x — implying a share price of DKK 133. He also includes a detailed trade receivables analysis with quarterly data from Q1 2021 to Q3 2023. Source: “Carnegie Research.”

Page 4: Signed: “Lars Topholm, Head of Research, Carnegie Investment Bank.” Full contact details: Overgaden neden Vandet 9B, DK-1414 Copenhagen K. Telephone, direct line, mobile, fax. www.carnegie.dk. Filial af Carnegie Investment Bank AB (publ), Sverige. CVR No 35541267. Reg. No 516406-0138. Standard Carnegie disclaimer footer about confidentiality and privileged material.

Let me say that again.

The document that Topholm calls “back of the envelope” is signed with his full title and Carnegie’s full corporate identity, CVR number, and legal entity registration. It contains revenue projections to DKK 1 billion, two valuation matrices with six EV/EBITDA scenarios each, a complete five-year P&L, EPS estimates, PEG ratio analysis, and quarterly receivables tracking.

This is not a napkin sketch. This is a Carnegie Research product. Branded, signed, distributed to the sales team and external investors. The regulator agreed. Finans.dk agreed. The only person still calling it “back of the envelope” is the man who wrote it — because calling it what it actually is would make what he did next look exactly like what it is.

Second: follow the money from the note to the bankruptcy

Here is the chain of causation that Finans.dk’s article did not trace:

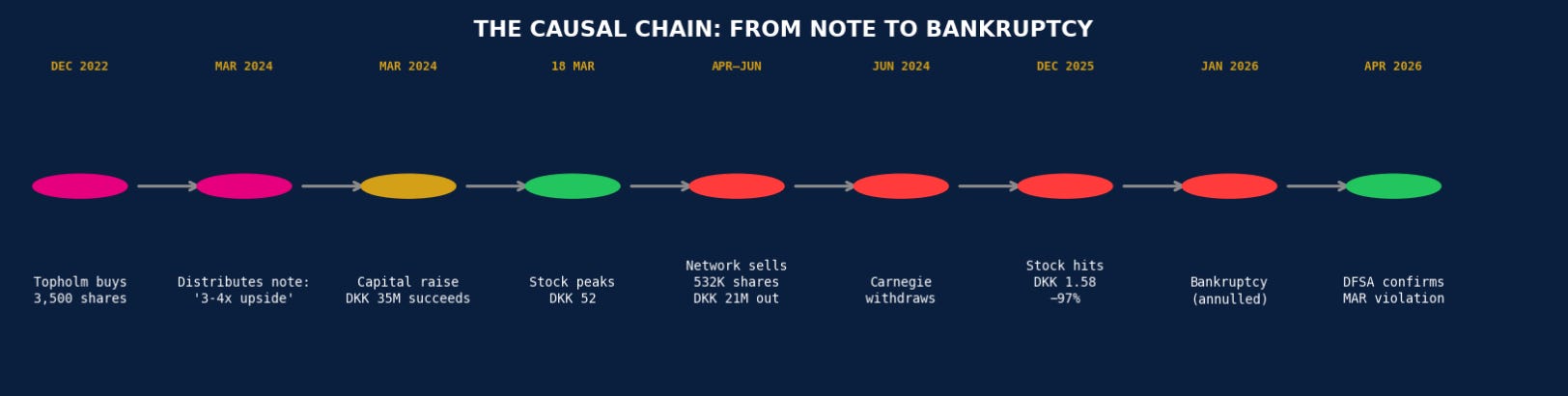

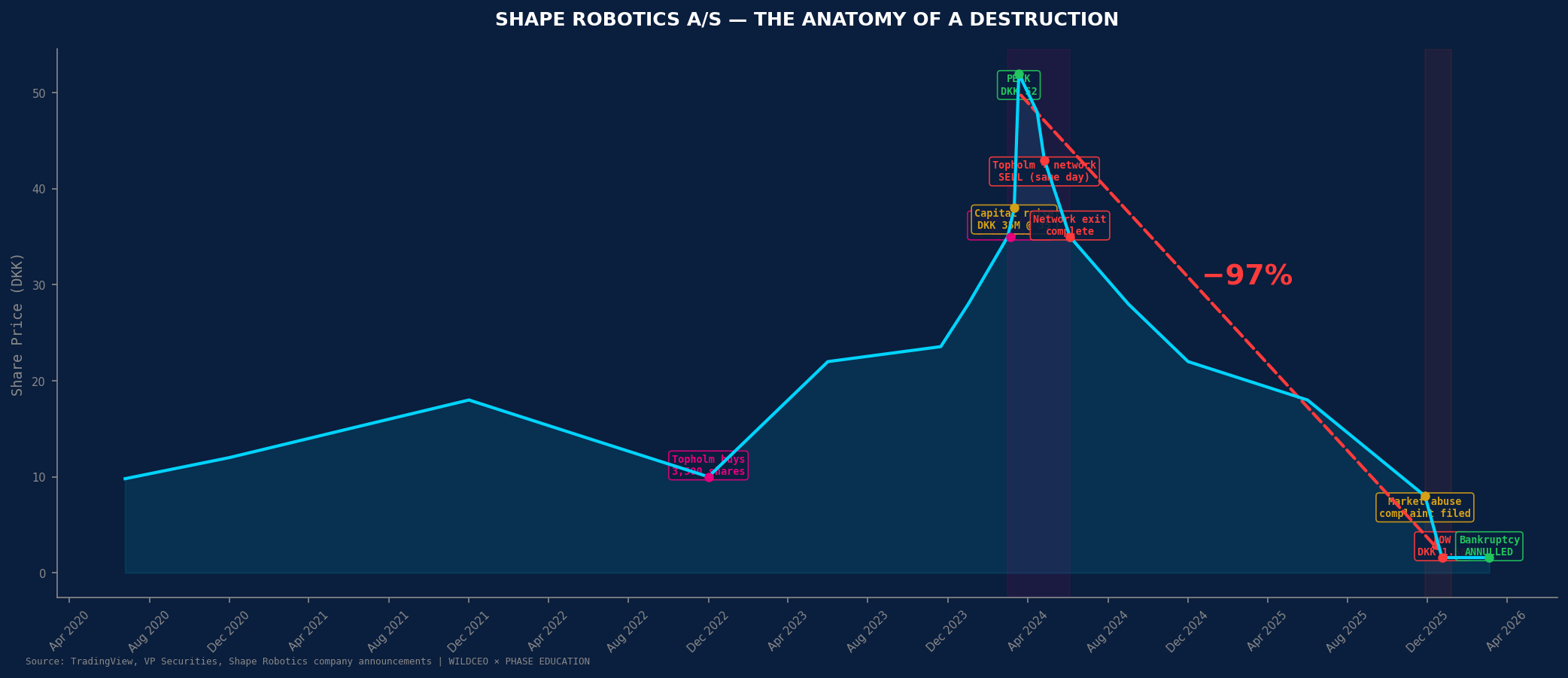

December 2022. Topholm buys 3,500 shares in Shape Robotics. Discloses this to no one.

5 March 2024. Topholm distributes the note. Opening line: “Looking for a micro cap idea where there is a theoretical argument for a 3-4x higher share price over the coming years?” Distributed to Carnegie’s internal sales team and to external investors.

11 March 2024. Shape Robotics raises DKK 35.4 million at DKK 35/share. Subscription indications exceed DKK 40 million. The raise succeeds — in a micro-cap where one analyst’s word is the entire market.

18 March 2024. Stock peaks at DKK 52. One week after placement at 35. A 49% premium. The note projected DKK 46.7–131.3 as “theoretical” value. DKK 52 lands right in the middle of his lower scenario.

15–16 April 2024. According to Mark Abraham’s documented account, Topholm attends private advisory meetings. Obtains non-public information: cash flows, Poland pipeline (€35M in government contracts), capital structure.

16–24 April 2024. Carnegie’s sales team — Topholm’s department — promotes Shape Robotics to institutional investors. Abraham cites a transcript: “We would have primed some of the key guys and that would have been Lars doing that.”

24 April 2024. Topholm emails the Chairman: “I allow myself to turn as a concerned shareholder and nothing else.” CC’s Martin Bundgaard — his self-described “best friend” — who holds 318,311 shares with no company role.

26 April 2024. Topholm sells all 3,500 shares. Same day, Sundvænget (network investment vehicle) sells 94,927 shares.

24 April – 4 June 2024. Network exits entirely. ~532,000 shares. ~DKK 21 million extracted at DKK 42–45.

6 June 2024. Carnegie withdraws. Two days after the last associated party finishes selling.

11 July 2024. Abraham records Topholm at breakfast: “I consider myself an insider. I can’t talk to anyone.” And: “Martin is my best friend. I speak to him anytime.”

June 2024 – Nov 2025. Without Carnegie’s support, the stock drifts. EIFO pulls loan guarantees. Liquidity evaporates. The capital structure, stressed by the post-raise hangover, begins to crack.

27 November 2025. Shape Robotics files a formal market manipulation complaint with Nasdaq.

28 November 2025. The DocuSign that triggers bankruptcy proceedings.

December 2025 – January 2026. Finans.dk publishes 17+ articles. Stock collapses to DKK 1.58.

6 January 2026. Bankruptcy decreed through defective service of process. Trustee writes DKK 199M in assets to zero. 70 jobs eliminated across five countries.

5 March 2026. Eastern High Court unanimously annuls the bankruptcy.

7 April 2026. Finanstilsynet confirms the Article 20(1) violation.

From the DKK 52 peak to DKK 1.58: a 97% destruction of shareholder value. DKK 205 million lost by 4,800 investors. And it started — not metaphorically, but factually, traceably, documentably — with a branded Carnegie Research note whose author held undisclosed shares.

Third: look at who held what — and what Finans didn’t tell you

Finans reported that Topholm’s shares were worth “omkring 130.000 kr.”

That is like reporting that the driver of a getaway car had €50 in his pocket while ignoring the €3 million in the trunk.

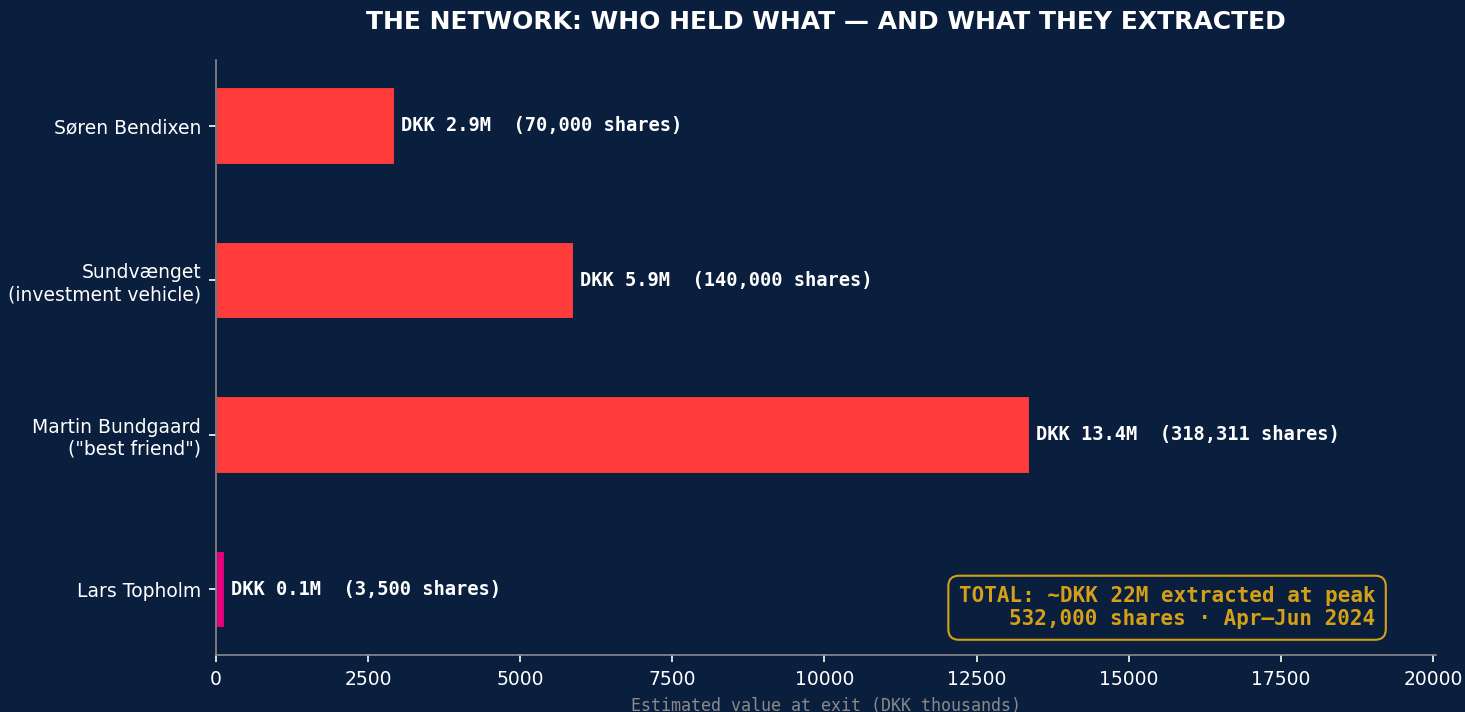

The DKK 130,000 is Topholm’s personal holding — 3,500 shares. Here is the full picture, as documented by Abraham from VP Securities records:

Martin Bundgaard — Topholm’s “best friend,” on tape — held 318,311 shares. At DKK 42: ~DKK 13.4 million.

Sundvænget — the network’s investment vehicle — held ~140,000 shares. At DKK 42: ~DKK 5.9 million.

Søren Bendixen — held ~70,000 shares. At DKK 42: ~DKK 2.9 million.

Total network position: ~532,000 shares. Total estimated extraction: ~DKK 22 million.

Finans reported DKK 130,000. The actual figure was approximately 170 times larger.

And then there is Fredericiagade Holding ApS — Søren Bendixen’s holding company, public in the Danish Business Registry. Profits: DKK 357,000 in 2022. DKK 37.2 million in 2024. A 10,320% increase during the exact period of the scheme. If Bendixen’s Shape exit was ~DKK 3 million, where did the other DKK 34 million come from?

“The mildest sanction” — or the maximum the system produces?

Finans calls the reprimand “den mildeste sanktion.” Let me reframe this with the regulator’s own enforcement data.

In 2023, Finanstilsynet opened 260 market abuse cases. Of 55 disclosure cases: 2 reprimands. Zero fines. Zero criminal referrals.

A reprimand is not the mildest sanction. A reprimand is the harshest outcome the system routinely produces for disclosure violations. The system does not fine analysts. It does not prosecute them. It does not name them. In the entire history of Danish regulation, the number of sell-side analysts fined for Article 20(1) violations is, as far as available records show, zero.

By comparison: a retail investor got 60 days’ imprisonment for nine wash trades in one month. The #1 analyst in the Nordics distributes an undisclosed-conflict recommendation preceding a DKK 35M capital raise and a 97% collapse: a reprimand.

When Finans tells you the punishment is mild, what they are actually telling you is that the system is mild. And a system where the Head of Research at Carnegie receives the same sanction as a blogger who forgot a disclaimer is not protecting investors. It is protecting insiders.

“No price effect” — the most dishonest phrase in the article

Finans reported the note “ikke havde en kursmæssig effekt.” The regulator explicitly stated this was legally irrelevant — the violation is the non-disclosure itself.

But beyond the legal point, the factual claim is absurd.

The note projects DKK 46.7–131.3 as theoretical value. It is distributed to Carnegie’s sales team and external investors in early March 2024. One week later, Shape Robotics raises DKK 35.4 million. The stock hits DKK 52.

If the note from the #1-ranked analyst in the Nordics — distributed through Carnegie’s institutional channels during a live capital raise — had “no price effect,” then his nine consecutive Extel rankings are a fraud. You cannot be the most influential analyst in Scandinavia and simultaneously have no influence.

“He sold when the price was falling” — a 400% profit reframed as a loss

Finans wrote: “Han solgte sine aktier i april 2024. På det tidspunkt var kursen faldet.”

Topholm bought in December 2022 at prices below DKK 10. He sold on 26 April 2024 at ~DKK 42–45. That is a 400–500% return. The stock had pulled back 15% from the DKK 52 all-time high. It was not falling — it was at the highest sustained level in the company’s history.

Framing this as “kursen var faldet” — the price had fallen — makes it sound like he was cutting losses. He was cashing out a four-to-five-fold profit. While his bank was still telling retail investors to buy.

What the note reveals about intent

This is where the document becomes the evidence.

The note opens: “Looking for a micro cap idea where there is a theoretical argument for a 3-4x higher share price?”

This sentence is not analysis. It is a pitch. It is designed to make the reader lean forward. And it was written by a man who, at that moment, held undisclosed shares in the company he was pitching.

The note then builds the case for that 3-4x upside using: revenue projections to DKK 1,023M by 2027, two valuation matrices covering six EV/EBITDA scenarios each, a complete P&L model, EPS estimates of DKK 4.44 (from DKK 0.18), and a PEG-ratio cross-check suggesting DKK 133.

The note is signed with Carnegie’s full corporate identity. Every table says “Source: Carnegie Research.”

And then the disclaimer on page 4: “Take it for what it is. This isn’t official research just a back-of-the-envelope so risk to the numbers stated above may be significant.”

This disclaimer is the forensic signature. A 33-year veteran, the Head of Research at Carnegie, who has signed off on thousands of compliant research reports, chooses to label this one as “unofficial” — while branding it with Carnegie’s name, distributing it through Carnegie’s channels, and signing it with Carnegie’s contact details and CVR number.

Why would the #1 analyst in the Nordics produce a document that looks exactly like a research note, functions exactly like a research note, is branded exactly like a research note — but label it “unofficial”?

Because if it is official research, Carnegie’s compliance framework kicks in. Personal holdings must be disclosed. The note must go through compliance review. The conflict of interest must be flagged.

If it is “just a back-of-the-envelope” — well, maybe the rules don’t apply.

The disclaimer is not a defence. The disclaimer is the smoking gun. It is the #1 analyst’s attempt to build plausible deniability into a document he designed to move money — while hiding the fact that the first money it would move was his own.

The three explanations — and why “mild” isn’t one of them

He’s incompetent. The #1-ranked analyst in the Nordics for nine years doesn’t know the first rule of compliance: disclose when you own the stock. If this is true, every Extel ranking is a fraud. Every institutional mandate based on Carnegie research was misplaced. Every compliance framework he supervised was supervised by a man who doesn’t understand compliance.

He’s expired. He knew the rules once but stopped caring. The simultaneous Aerbio chairmanship (seeking €50M from the same investor pool), the personal trading in covered stocks, the “unofficial” disclaimer on a branded Carnegie note — a man who has been told he is the best for a decade stops hearing the word “no.”

He’s corrupt. The non-disclosure was deliberate. The “back of the envelope” label was cover. The timing — note → capital raise → peak → confidential meetings → network sells → Carnegie withdraws → collapse — was a sequence, not a coincidence. The DKK 22 million extracted by his network at the peak was the objective, not a side effect.

It doesn’t matter which explanation you choose. Every one of them means the same thing: Carnegie’s compliance systems either failed or were never designed to work. The Danish regulatory system either cannot detect this or does not want to. And 4,800 shareholders paid for both failures with DKK 205 million.

The question every Carnegie client should ask — and the one Finans didn’t

Lars Topholm covered Novozymes, Chr. Hansen, NKT, Nilfisk for 20+ years. His research moved billions. The regulator just confirmed he violated disclosure rules on Shape Robotics.

Was Shape Robotics the only time?

People do not develop new character traits at the apex of their career. They reveal the character they have always had.

And the question Finans.dk did not ask — while listing Abraham’s lawsuits as if the volume of complaints discredits the complainant rather than reveals the scale of the problem — while failing to disclose that Shape Robotics is suing Finans.dk’s own parent company for EUR 14 million:

If you considered yourself an insider — your words, on tape, at Villa Copenhagen — why did you sell?

The reprimand is not the story. The reprimand is the receipt. It is the government-stamped proof that the man at the centre of a DKK 205 million destruction was operating outside the law from the beginning.

You do not get to call it mild. You do not get to call it closed. And you do not get to frame the man who uncovered it as the problem.

Q.E.D.

Sources

Mark Abraham — CEO, Shape Robotics A/S · Creator, Phase Education · Born in Romania

#ShapeRobotics · #WildCEO · #GameOver · #LarsTopholm · #Carnegie · #PumpAndDump