Fifty-five days into a war I didn’t start. Ten days until the court hearing on 11 May.

Today on the livestream I tried something new: a one-on-one Friday format with Jørgen Andreas Berg as co-host. Jørgen is finishing his bachelor’s in business in Norway, has been collecting signatures on the Nordnet thread, and today filed petitions on behalf of approximately 30 shareholders.

He brought the questions. The hardest ones from the Nordnet thread. I answered them on stream, with documents on screen. This dispatch is the structured version, with the two contractual exhibits I shared publicly for the first time.

❶ Q: “Sanako was profitable but couldn’t pay salaries — and now two parties accuse Shape Robotics of stealing EUR 4.5M abroad. What really happened?”

The question is structured to imply a contradiction. There is no contradiction. There are four logical errors in the framing.

🎯 Logical error one — profitability ≠ liquidity.

Sanako Oy was profitable: 50.6% operating margin, 72% equity ratio, EUR 2M revenue in FY2024 (Suomen Asiakastieto public registry). Profitable. Period.

Sanako Oy lacked cash. It lacked cash already when we acquired it in June 2025 — that was one of the reasons we acquired it via share swap rather than cash. A profitable company can simultaneously have temporary cash flow constraints. That is corporate finance 101. Confusing the two is not a discovery — it is a misreading.

🎯 Logical error two — there are not two independent parties accusing.

Per the company’s own publicly filed announcement of 11 March 2026: “Mr. Gullitz-Wormslev was copied on the Finnish administrator’s communications from the start.” Per Cision Announcement 07-26 of 24 March 2026, the Finnish pesänhoitaja from Asianajotoimisto Ylikraka Oy is described as the liquidator’s “colleague.”

Two coordinating voices are one narrative. The arithmetic of independent corroboration does not apply when the corroborators communicate from the start.

🎯 Logical error three — buying a company to consolidate cash flow is not a crime.

Cash pooling between a parent and a 100%-owned subsidiary is the global standard treasury structure. Selskabsloven § 222 permits inter-group transfers serving commercial purpose. IFRS 10 consolidates them automatically. Every multinational group on Nasdaq Copenhagen does this — Maersk, Carlsberg, Novo Nordisk, all of them.

Sanako was acquired in June 2025 through share swap with a § 160 valuation report at EUR 8.6M. We used illiquid Shape A/S shares — paralyzed by the November 2024 pump-and-dump that crushed the share price — to acquire a profitable European company that could be consolidated under IFRS 10 and then attract new financing for the EUR 40M Polish PNRR pipeline (Bechtle contract). That is exactly what M&A is for.

🎯 Logical error four — Sanako was paying salaries until Teis arrived.

Here is the simplest test of the accusation. How did Sanako Oy pay salaries in December 2025 — and then suddenly fail to pay them in January 2026, exactly when Teis became kurator with shareholder authority over Sanako?

The 100% shareholder representative on 5 February 2026 — when Sanako filed the voluntary bankruptcy petition — was Teis Gullitz-Wormslev. He had the authority to move group cash. He had the authority to call in customer payments. He had the authority to authorize the Polish project that would have generated immediate revenue. He chose not to. Then he allowed the bankruptcy filing.

If he believed cash had been improperly extracted from Sanako, he had thirty days as kurator with full legal authority to recover it. He did nothing. His behavior contradicts his accusation.

The accusation is therefore not just wrong on the facts — it is structurally incoherent. It accuses one person of misconduct while describing actions that only the accuser had legal authority to remedy.

❷ Q: “Will you share the auditor’s resignation letter from Beierholm?”

Yes. I shared it live on screen today.

The letter is dated 18 December 2025, signed by Thomas Thomsen, partner at Beierholm. It reads:

“Dear Mark and Aurel,

I am sorry to inform you that we have decided to resign as Auditor of Shape Robotics A/S. Our resignation is due to lack of communication with and trust in the company’s management.

We are obliged to notify the Danish Business Authority and Nasdaq of our resignation and the reason for it, which will be done immediately following this email.

We have communicated with Nasdaq about this issue. They have asked me to inform you that you are obliged to inform the market about our resignation.”

That is the entire letter. No specific concerns cited. No findings. No referenced transactions. “Lack of communication with and trust in the company’s management” — that is the stated reason.

🎯 Same date as the Finans.dk article.

On 18 December 2025 — the exact day Beierholm resigned — Finans.dk published an article titled “Mark Abraham anmeldt for grov bedrageri i ikke-konkursramt selskab i Rumænien” (translation: “Mark Abraham reported for gross fraud in non-bankrupt company in Romania”).

Same day. The auditor was scared by the media coverage. Last week, in a private conversation, Thomsen confirmed it directly to me: the reason he decided not to continue was the Finans articles.

That is what happened to the auditor. Not an audit finding. A media scare.

The fraud allegation referenced by Finans.dk is the subject of an ongoing legal dispute. We are pursuing Finans.dk in court for the November-December 2025 coverage. The allegation has not been proven — and “reported for fraud” is not the same as “found guilty of fraud” under any legal system. But that is the article that triggered Beierholm’s resignation.

We are now looking for an international auditor with the capacity to operate independent of small-market Danish media pressure. The Danish audit market is too small. An international firm is the right call.

❸ Q: “Will you share the Earn-out terms from the Story Kids acquisition?”

Yes. I shared two pages on screen. They are reproduced below in full.

Exhibit A — Warrant Agreement (2021, acquisition year)

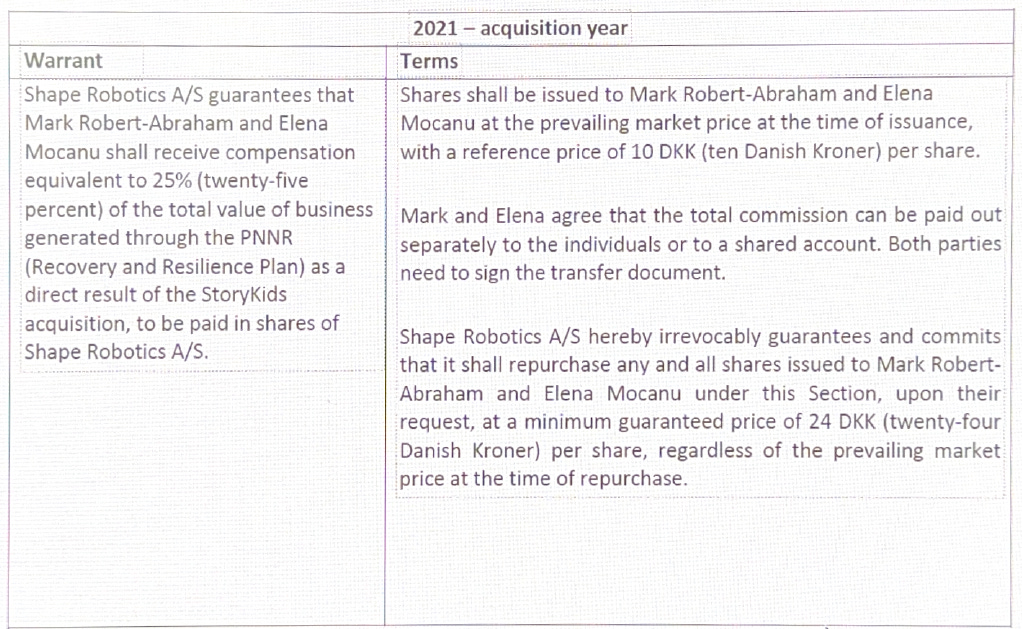

Warrant: “Shape Robotics A/S guarantees that Mark Robert-Abraham and Elena Mocanu shall receive compensation equivalent to 25% (twenty-five percent) of the total value of business generated through the PNRR (Recovery and Resilience Plan) as a direct result of the StoryKids acquisition, to be paid in shares of Shape Robotics A/S.”

Terms: “Shares shall be issued to Mark Robert-Abraham and Elena Mocanu at the prevailing market price at the time of issuance, with a reference price of 10 DKK (ten Danish Kroner) per share. Mark and Elena agree that the total commission can be paid out separately to the individuals or to a shared account. Both parties need to sign the transfer document.

Shape Robotics A/S hereby irrevocably guarantees and commits that it shall repurchase any and all shares issued to Mark Robert-Abraham and Elena Mocanu under this Section, upon their request, at a minimum guaranteed price of 24 DKK (twenty-four Danish Kroner) per share, regardless of the prevailing market price at the time of repurchase.”

That is the document signed in 2021 at the time of the Story Kids acquisition. Two key elements:

✓ Compensation equal to 25% of PNRR business value, paid in Shape A/S shares

✓ Repurchase guarantee at 24 DKK per share — irrevocable, by Shape A/S, regardless of prevailing market price

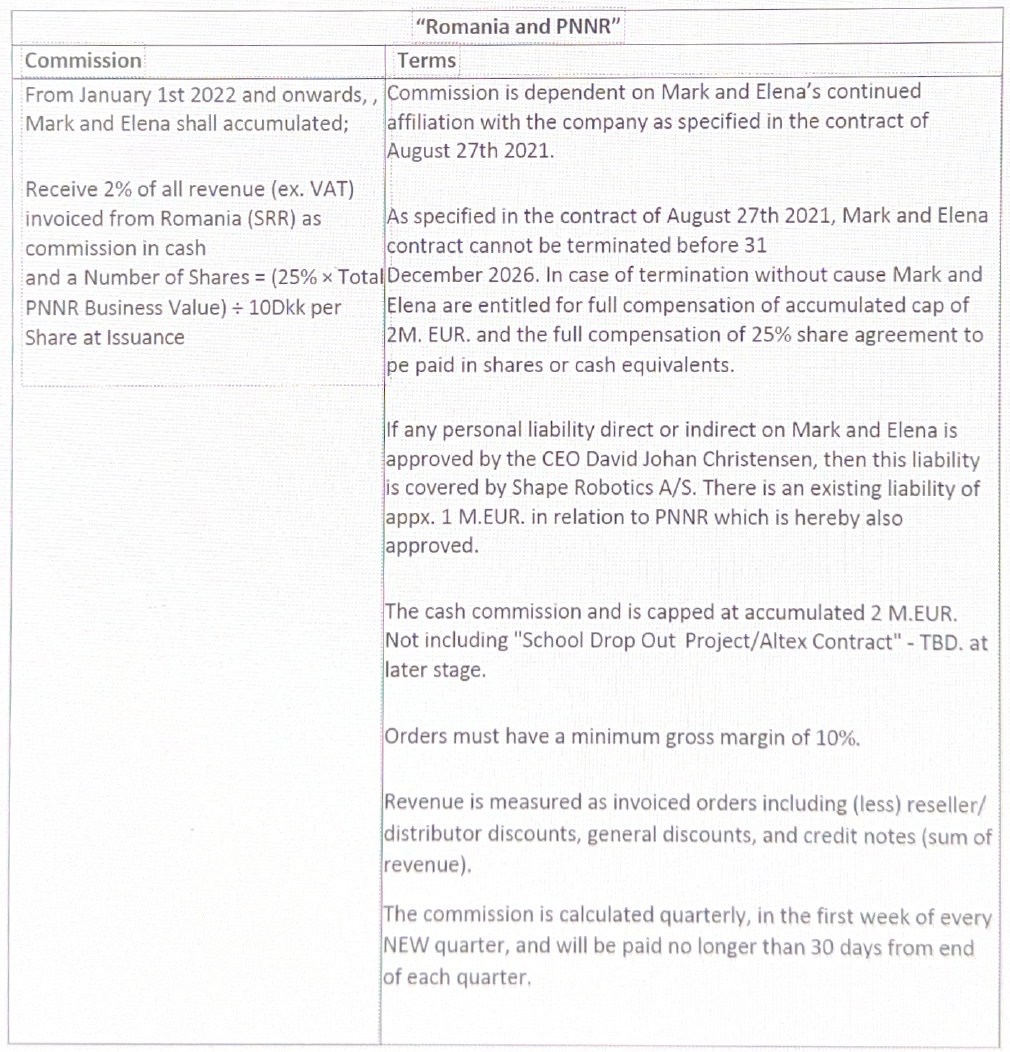

Exhibit B — Commission Terms (effective 1 January 2022)

Commission: “From January 1st 2022 and onwards, Mark and Elena shall accumulate: receive 2% of all revenue (ex. VAT) invoiced from Romania (SRR) as commission in cash AND a Number of Shares = (25% × Total PNRR Business Value) ÷ 10 DKK per Share at issuance.”

Terms (excerpts):

“Commission is dependent on Mark and Elena’s continued affiliation with the company as specified in the contract of August 27th 2021.

As specified in the contract of August 27th 2021, Mark and Elena’s contract cannot be terminated before 31 December 2026. In case of termination without cause Mark and Elena are entitled for full compensation of accumulated cap of 2M EUR and the full compensation of 25% share agreement to be paid in shares or cash equivalents.

If any personal liability direct or indirect on Mark and Elena is approved by the CEO David Johan Christensen, then this liability is covered by Shape Robotics A/S. There is an existing liability of appx. 1 M.EUR in relation to PNRR which is hereby also approved.

The cash commission is capped at accumulated 2 M.EUR (Not including ‘School Drop Out Project / Altex Contract’ — TBD at later stage). Orders must have a minimum gross margin of 10%. Revenue is measured as invoiced orders... The commission is calculated quarterly, in the first week of every NEW quarter, and will be paid no longer than 30 days from end of each quarter.”

Two contractual mechanisms are visible here:

✓ A 2% cash commission on Romanian revenue, capped at EUR 2M cumulative

✓ A 25% share component of total PNRR business value, in Shape A/S shares at 10 DKK reference price, converting to cash equivalent if termination without cause occurs

The “termination without cause” clause is the core mechanism. Bankruptcy, liquidation, hostile removal of management — all qualify. When the share-conversion mechanism becomes unavailable (because the company collapsed), the contract converts the share entitlement to cash equivalent.

That is what crystallized on 6 January 2026. Not a number filled into a blank cheque. A contractual condition triggering a contractual remedy.

I will retain certain operational details — specific revenue figures, the full SPA, the side-letters — until 11 May 2026, for litigation strategy reasons. The two pages above are the structural skeleton. They show what the deal was. They show what the trigger was. They show what the remedy is.

❹ Q: “Why is none of this in the annual reports?”

Because the structure is a contingent commitment, not a booked liability — until the trigger event occurs.

The accounting position throughout 2022-2024 was:

✓ Mark and Elena receive a 2% cash commission on invoiced Romanian revenue, capped at EUR 2M — paid quarterly, expensed quarterly, recorded in the year of accrual

✓ Mark and Elena hold a share entitlement equal to 25% of accumulated PNRR business value — convertible into Shape A/S shares at 10 DKK reference, with the share-conversion mechanism active as long as the company functions normally

As long as the share mechanism is operative, no DKK liability appears on the balance sheet — the obligation is satisfied through equity dilution at issuance. Equity-settled obligations are accounted for differently from cash-settled obligations under IFRS 2. They are disclosed in note form, not booked as financial debt.

🎯 The conversion to cash liability happens only when share-settlement fails.

Bankruptcy makes share issuance impossible. The fallback engages. The cash equivalent crystallizes. That happens on the date of the triggering event, not retroactively across prior accounting periods.

The accounting treatment is consistent with how earn-out share-based instruments are treated across European listed issuers. Was the disclosure adequate? That is a fair question, and one I would welcome an independent reconstructor or the Erhvervsstyrelsen audit committee to examine. I will not litigate the disclosure question on Substack. The reconstructor on 11 May has the file.

What the critic has misread is this: Story Kids brought EUR 88 million of business into Shape Robotics through the Romanian subsidiary. The 25% commission on the PNRR component of that business was always a contractual entitlement — but as long as the share-settlement mechanism worked, it was an equity-instrument disclosure, not a cash-debt entry.

Bankruptcy broke the share mechanism. The cash entitlement materialized. That is the entire mechanic.

❺ Q: “And EIFO? What about the state development fund?”

I shared the breaking news live today. EIFO will be paid in full. That is a public commitment.

We have a bridge financing facility in the final stages of preparation:

✓ Up to USD 3 million total, with first tranche of USD 750,000

✓ Up to 18 months tenor, 12% per annum, with conversion right at 15%

✓ Secured by a first-ranking charge over Shape A/S assets and current/future subsidiaries

✓ Expected closing in May 2026, conditional on reconstruction commencing

✓ I personally guarantee the first USD 750,000 unconditionally

The plan is straightforward: reconstruction begins on 11 May, the bridge facility closes within the first week, EIFO is repaid in full from the proceeds, the floating charge is released, and the operational company continues with a clean senior debt structure.

🎯 Why EIFO matters specifically:

EIFO is the Danish state’s export and investment fund. Their mandate is to support Danish exporters operating internationally. We are exactly the kind of company they were created for — a Danish technology exporter selling to schools across Eastern Europe and Asia.

Whatever the historical defaults issue between EIFO and Shape A/S — most of which preceded my time as CEO and which I cannot relitigate here — the path forward is to honor the obligation in full. EIFO gets paid. State capital is preserved. The operational company survives. That is the only outcome that serves everyone.

We are not trying to write down EIFO’s claim. We are trying to pay it.

❻ Q: “If the company was profitable in 2024 with EUR 88M business through Story Kids, why are we even in this situation?”

Because of the pump-and-dump in November 2024 that destroyed the value of the share currency.

Here is the sequence that the critics keep ignoring:

2021-2024: Shape Robotics A/S consolidates Story Kids, builds the EUR 100M PNRR pipeline through Shape Romania, executes successfully. Revenue grows. Margins grow. Operations are healthy.

November 2024: A coordinated short-selling and negative-coverage campaign — what we call the pump-and-dump, with documented activity from Lars Topholm at Carnegie and persistent negative coverage from Finans.dk — crashes the share price. The DKK 24 per share repurchase guarantee in our 2021 contract becomes unenforceable in practice because no fresh share issuance can be done at price levels that wouldn’t destroy the cap table.

December 2024 – November 2025: We attempt to fix the situation through the IRIS equity facility, the Aurel share purchase, the move to Main Market on Nasdaq Copenhagen, the Sanako share-swap acquisition, the EUR 40M Polish Bechtle contract.

November 2025: We come clean publicly about the pump-and-dump. The auditor resigns under media pressure on 18 December.

6 January 2026: Bankruptcy decree by Sø- og Handelsretten — issued without proper service to me as CEO, and unanimously annulled by Østre Landsret on 5 March 2026.

🎯 The critical point: We were never bankrupt. We had liquidity tightness. We had been damaged by the pump-and-dump. We had been abandoned by the auditor. The board had been disrupted. But we were not bankrupt.

If we had been properly served on 6 January and given the chance to defend Shape A/S in court, no court would have bankrupted the company. We were recovering. We had just made tabula rasa on the stock exchange. We had filed the IRIS equity line. The Polish project was signed.

The destruction of value happened during the unlawful trustee period — 6 January to 5 March 2026 — not before it. That is what the trustee is now trying to obscure by attacking pre-bankruptcy management decisions.

The reconstruction on 11 May restores the path. The bridge facility activates. EIFO is paid. The schools’ subscriptions are honored. The operational company survives.

That is the whole story, in five paragraphs.

✊ Where the petition stands tonight

Jørgen filed petitions today on behalf of approximately 30 shareholders via the Nordnet thread. The shareholders’ petition is now formally consolidated. The supplementary complaint is with Finanstilsynet. The criminal complaint is with Københavns Politi.

🗓️ Deadline for additional signatures: Saturday 2 May 2026, 23:59 CET 🚀 Filing of consolidated petition: Monday 4 May 2026, morning 🏛️ Court hearing: Sunday 11 May 2026, 09:30 — Sø- og Handelsretten

Bo coordinates in-person attendance in Copenhagen. If you can be there — be there.

🔚 Closing

I told Jørgen on stream today: I do not want to come back as CEO. I do not want to be famous. I do not want to be rich from this.

What I want is to come back to pre-pump status. I want the company we built to function. I want the EUR 100M PNRR pipeline to deliver. I want the schools to use the robots they paid for. I want the platform to work in classrooms across Eastern Europe.

The 99.99% haircut is the public commitment. EIFO gets paid. The platform runs. Mazanti-Andersen’s Philip Borreschmidt examines every claim independently. Whoever the independent reconstructor finds is right is right. Whoever they find is wrong is wrong.

I accept independent assessment. I have been asking for it for fifty-five days.

11 May. Independent reconstructor. Q.E.D.

Mark-Robert Abraham · Founder and former CEO, Shape Robotics A/S · 1 May 2026 · Day 55

Co-host today: Jørgen Andreas Berg — lead complainant on the shareholders’ petition · joergen.andreas.berg@gmail.com

🤖 Wild CEO AI agent — trained on the full case archive — at wildceo.live.

📎 Embedded in this dispatch: Warrant Agreement (2021) and Commission Terms (effective 1 January 2022) from the Story Kids acquisition file. Additional documents released under controlled litigation strategy ahead of 11 May.

🏷️ #ShapeRobotics #PhaseEducation #NasdaqCopenhagen #SHAPE #BiletLaOrdin #PromissoryNote #Aval #StoryKids #PNRR #EUR88M #Earnout #Warrant #IFRS2 #IFRS10 #CashPooling #Selskabsloven #Sanako #SøOgHandelsretten #ØstreLandsret #KromannReumert #TeisGullitzWormslev #Tvangsopløsning #Likvidator #Reconstruction #MazantiAndersen #PhilipBorreschmidt #Independence #JørgenAndreasBerg #ShareholderPetition #Beierholm #FinansDK #PumpAndDump #LarsTopholm #EIFO #DanskeBank #BridgeFinancing #SchoolsFirst #WildCEO #GameOver #Day55 #FridayQA