GAME OVER | Day 37: 18 Questions and One They Won’t Answer

Nasdaq sent me a 14-page investigation letter. Unsigned. Marked “Internal Use.” I sent back 47 pages — signed, cited, and copied to Finanstilsynet.

Previous episodes: Day 36: The Door Is Open | Day 35: “This Is Not Negligence” | Day 34: The Regulator Agrees | There Is No “Mild” Version of This | The Man Who Knew the Rules

Day 37 since the Danish High Court unanimously annulled the bankruptcy of Shape Robotics.

Trading is still suspended.

4,800 shareholders still cannot sell. Still cannot buy. Still cannot do anything with shares they own in a company that is alive, operational, and fighting.

Today I am publishing the full Nasdaq response because I am done asking politely. You, the shareholders, deserve to see exactly what is happening behind the curtain. Every word. Every question they asked. Every answer I gave. And the one question they refuse to answer.

What arrived at 10:21 this morning

At 10:21 Copenhagen time, Nasdaq Surveillance sent me a 14-page letter titled:

“Nasdaq investigation of non-compliance with and potential breaches of Nasdaq rules — Request for an explanation”

Eighteen questions. Fourteen pages. Addressed to the CEO and to Aurel Nețin.

Unsigned. No physical or electronic signature. Marked “Nasdaq — Internal Use: Distribution limited to Nasdaq personnel and authorized third parties subject to confidentiality obligations.” Sent by plain email, with no authentication, no certification, no legal stamp.

This is what a regulated European exchange considers formal regulatory correspondence with a listed issuer. An unsigned internal memo, telling us not to share it with anyone.

I responded with 47 pages. Signed. Referenced. Cited. Every annex attached. Copied to Finanstilsynet.

And then I published this.

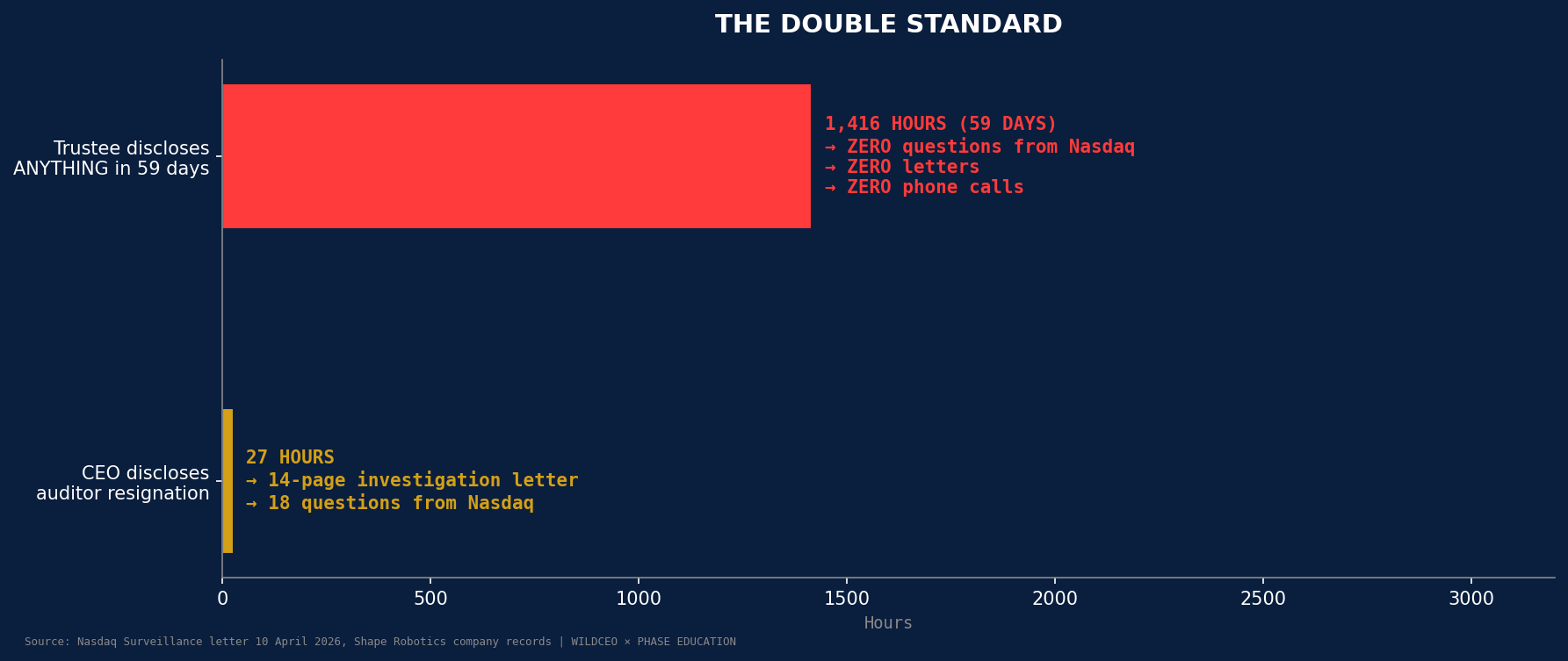

Nasdaq asked about 27 hours. They forgot about 59 days.

This is the table I put in my response to Nasdaq. I wanted them to see it in black and white. Now I want you to see it too.

The Company was informed of the auditor’s resignation at 13:07 on 18 December 2025. The CEO responded within 19 minutes. The disclosure was published the following business day at 15:54.

Twenty-seven hours. That is what Nasdaq considers a problem.

The trustee — Teis Gullitz-Wormslev of Kromann Reumert, Denmark’s largest law firm — had sole control of Shape Robotics for 59 days. Full access to every system. Every bank account. Cision. VP Securities. Digital Post. Everything.

In fifty-nine days, the trustee published zero company announcements.

During those fifty-nine days: the Finnish subsidiary Sanako Oy was pushed into bankruptcy — EUR 9 million destroyed. Company funds were redirected to Kromann Reumert’s own client account — DKK 568,700. The Extraordinary General Meeting was cancelled — blocking a EUR 15 million equity facility. DKK 3.7 million was deposited in a Nordea escrow account registered in Kromann Reumert’s name — six days after the mandate was annulled by the High Court.

4,800 shareholders were told nothing. For fifty-nine days.

Nasdaq knew. Nasdaq watched. Nasdaq did not send the trustee a single letter. Not one question. Not one phone call. Not one unsigned internal memo.

I took 27 hours to assess an auditor’s unilateral resignation, prepare a MAR-compliant announcement, and publish it through Cision — all while operating with a collapsing board and no prior warning. They wrote me 14 pages about it. The trustee published nothing for 1,416 hours. They wrote him zero.

The 18 questions — translated for people who don’t read EU regulations for fun

Nasdaq’s letter is technically dense. It cites Rule 3.1.1, MAR Article 17, Supplement A Part C Rule 13, Rule 2.15.3(b), Rule 3.5.2, Rule 3.2.1, Rule 3.11.1, and Rule 4.2.1. It references ESMA standards, OAM submissions, and categorization requirements.

Let me translate what they actually asked and what I actually answered. Because you should not need a securities law degree to understand what is being done to your investment.

“When did you know there was going-concern risk?”

Nasdaq’s framing implies that we hid financial distress. Here is the truth.

The financial difficulty began when EIFO pulled the credit guarantees in June 2024 — after the former board’s negligent uplisting decision. The same uplisting that the DFSA has now indirectly confirmed was tainted by market abuse. The board that made that decision has resigned. I filed negligence claims against all of them. But Nasdaq didn’t ask the board. Nasdaq asked me.

And the Company had DKK 302 million in revenue in 2024. This was not a startup burning cash. This was a company with a structural liquidity problem caused by the actions of people Nasdaq has never questioned.

“Why did you take 27 hours to disclose the auditor’s resignation?”

Because that is how responsible disclosure works.

The auditor — PwC — resigned without warning at 13:07 on a Thursday afternoon. No prior discussion. No phone call. Just an email. By Friday afternoon — one business day later — the announcement was published on Cision, properly categorized under MAR, and paid for from my personal bank account because the company had no money.

Nasdaq’s letter helpfully includes my email response from 19 minutes after receipt:

“Can u please give us a break? Why you want to charge even more on us. Trust last time I have checked — trust is a subjective quality. At least have the decency to make a call with us”

Yes, I wrote that. I was running a company whose board had collapsed, whose chairman had just resigned, and whose auditor decided to email a resignation with no warning and no discussion. Nineteen minutes later, I responded in frustration. Twenty-seven hours later, I published a compliant announcement. That is what Nasdaq considers non-compliance.

“Why did you take 24 hours to disclose the IRIS LOI?”

Because on 11 March 2026 — six days after being reinstated by the High Court — I had: no access to Cision, no access to any company bank account, no support staff, no IR department, no communications team, no company email, no company stationery, and no access to any company system. Everything was held by the trustee who refused to return it.

The Cision announcement had to be purchased from my personal funds, drafted personally, formatted to MAR requirements personally, and submitted through a system I had to re-register for from scratch.

The LOI was disclosed within 24 hours. This was as soon as physically possible.

Nasdaq noted that the document I sent to Surveillance was “a draft version with non-removed track-changes and has not been signed by any party.” Of course it was. I had no access to a printer, a scanner, or company stationery. The former trustee had all of it. I was working from a personal laptop, with a personal email address, paying for announcements from a personal bank account.

Under these circumstances, the fact that the document had track-changes is not evidence of non-compliance. It is evidence of the extraordinary conditions under which the only person fighting for this company was operating.

“How many bankruptcy petitions are filed against you?”

I don’t know. And Nasdaq knows I don’t know. And Nasdaq knows why I don’t know.

No petition has been lawfully served on the Company since the annulment. The High Court annulled the original bankruptcy precisely because of defective service. The Company’s Digital Post access — which is how Danish courts communicate — is held by the former trustee who refuses to return it. I filed a criminal complaint about this (ref. 0100-83986-10362-26). I contacted the Maritime and Commercial High Court directly. I requested service under EU Regulation 2020/1784.

And here is the part that should make you pause: Nasdaq confirmed on 13 March 2026 that it was in direct contact with the Maritime and Commercial High Court. Nasdaq confirmed that petitions exist. Nasdaq had this information. The Company did not. And then Nasdaq criticized the Company for not disclosing information that only Nasdaq possessed.

I cannot disclose what I do not have. If Nasdaq wants the market to be informed, Nasdaq is free to share the information with me so that I can assess my disclosure obligations. Or Nasdaq can publish it itself. What Nasdaq cannot do is withhold the information, criticize me for not disclosing it, and then use my non-disclosure as justification for continued suspension.

The Finanstilsynet reprimand — the fact Nasdaq’s letter did not mention

Three days before Nasdaq sent me this letter, the Danish Financial Supervisory Authority published a formal reprimand confirming that the starting point of this entire chain of events — the analyst recommendation that pumped the stock, triggered the capital raise, and set up the collapse — was a violation of EU market abuse law.

Article 20(1) of the Market Abuse Regulation. Formal finding. Published on finanstilsynet.dk. Company Announcement No. 10-26 issued the same day.

The Danish regulator confirmed, in writing, that Shape Robotics was the victim of market abuse.

Nasdaq’s 14-page letter, dated three days later, does not mention it. Not once. Not in a footnote. Not in a passing reference. Not anywhere.

The regulator of the Danish capital markets has officially confirmed that the company Nasdaq is investigating was the victim of a crime committed by a third party. And Nasdaq’s investigation proceeds as if this did not happen.

Three periods — three leaderships — and Nasdaq conflates them all

Nasdaq’s letter covers events from October 2025 to April 2026 as if one continuous management were responsible. I put this in the response because the conflation is either ignorant or deliberate, and neither is acceptable from a regulated exchange.

Before 6 January 2026. The former Board of Directors — Frandsen, Rootzen, Lindgreen, Holst Hansen, Ikov — plus CEO Mark Abraham. All five board members resigned by November 2025. All disclosure decisions in this period were made by or with the former board. All five are now subject to a formal negligence claim (SR-NEG-2026-BOD).

6 January – 5 March 2026. Fifty-nine days. Trustee Teis Gullitz-Wormslev, Kromann Reumert. The Company under sole control of the trustee. Management had zero access to systems, bank accounts, Cision, VP Securities, email, financial records, or any company infrastructure. The trustee published zero company announcements. Nasdaq asked the trustee zero questions.

After 5 March 2026. CEO Mark Abraham reinstated by Østre Landsret, plus Aurel Nețin. Operating without any company records, systems, credentials, or infrastructure — all retained by the former trustee despite formal demands and criminal complaint.

The current management cannot answer for what happened during the 59-day bankruptcy. The trustee can. Nasdaq has not asked the trustee a single question. The current management has limited ability to answer for what happened before the bankruptcy. The former board can. They have all resigned and are the subject of a formal negligence claim.

Rule 4.2.1 does not say what Nasdaq claims it says

Nasdaq writes: “As a standard procedure according to rule 4.2.1 in Nasdaq’s rules, Nasdaq suspends trading in the event of a bankruptcy petition is filed.”

Here is the actual text of Rule 4.2.1:

“The Exchange may suspend an Issuer’s Shares from trading if the Issuer no longer complies with the Rulebook or if orderly trading in the Issuer’s Shares cannot be guaranteed.”

That is the entire rule. There are no sub-rules. No guidance text. No cross-references. And no mention of bankruptcy, bankruptcy petitions, insolvency, or any other specific triggering event. The rule provides only two discretionary bases: non-compliance with the Rulebook, or the inability to guarantee orderly trading. The word “may” grants discretion — it does not impose an obligation.

Nasdaq attributes language to the rule that does not exist in it. And then uses that invented language to justify a suspension that has lasted 37 days since the bankruptcy was annulled.

Under Kapitalmarkedsloven §78(1) — the Danish Capital Markets Act — and MiFID II Article 52(1), a suspension must not be carried out if it would cause significant damage to investors’ interests. With 4,800 shareholders locked out, a EUR 15 million facility blocked, and the company’s recovery actively impeded — that threshold is not theoretical. It is being crossed every day.

The circular prison — and why it matters to every small investor

I want to explain this because it is the most absurd part of the entire situation and nobody is talking about it.

Nasdaq suspends trading because of “bankruptcy petitions being processed.” These petitions have not been lawfully served on the Company. I don’t know who filed them, for what amounts, or on what basis. I have asked the court for proper service. I have asked Nasdaq — who confirmed they checked the court registry — to share the information. Nobody will give it to me.

But it gets worse.

To lift the suspension, I need to demonstrate that the company is operational, compliant, and financially viable. That requires capital. Capital requires investors. Investors require liquidity — meaning their shares need to be tradeable. Trading requires Nasdaq to lift the suspension.

Do you see the circle?

I cannot get capital because trading is suspended. Trading is suspended because I supposedly don’t have capital. And Nasdaq will not tell me what I actually need to do to break the circle.

Meanwhile, since 5 March 2026, I have: published 10 Company Announcements — all paid from my personal funds. Filed a D&O negligence claim. Secured a EUR 15 million binding letter of intent from IRIS Capital. Responded to every single Nasdaq inquiry within days. Filed criminal complaints against the trustee. Obtained a formal DFSA reprimand confirming market abuse. Scheduled an EGM for 14 April — new board, new auditor, 100 million shares authorized, rebranding confirmed.

The trustee, during 59 days of sole control, did none of this. Published nothing. Disclosed nothing. Returned nothing. And is the subject of zero Nasdaq questions.

The one question they won’t answer

Here is the part I put in red boxes at the top and bottom of my 47-page response. Here is the question I have asked every single day for 37 days.

WHAT ARE THE CONDITIONS FOR LIFTING THE TRADING SUSPENSION?

What do we need to do? What boxes do we need to check? What documents do we need to file? What approvals do we need to obtain? What threshold do we need to meet?

Tell us. Write it down. Send it to us. And we will do it.

We have asked this question since 5 March. In writing. In formal escalation letters. Through the Finanstilsynet complaint (ref. 25-026876). In every single communication with Surveillance.

The answer, every single time: silence.

If Nasdaq cannot state the conditions for resumption, then there are no conditions. And if there are no conditions, the suspension is arbitrary. And if the suspension is arbitrary, it is unlawful under Section 78(1) of the Danish Capital Markets Act.

I gave them until 23 April 2026. The Company demands: a written statement of the specific legal basis, a written list of conditions, a timeline for assessment, and a public market notice explaining the current basis to 4,800 shareholders.

What I told Nasdaq today — and what I asked them back

The full 47-page response answers all 18 questions. Every single one. In full. Transparently. With context, dates, evidence, and citations. The response also poses 8 counter-questions that Nasdaq has never addressed:

CQ-1. Why did Surveillance not demand any disclosure from the trustee during the 59-day bankruptcy?

CQ-2. Has Surveillance investigated whether the trustee’s 59-day silence breached MAR Article 17?

CQ-3. Why does the 14-page letter not mention the Finanstilsynet reprimand of 7 April — published three days before the letter?

CQ-4. On what legal basis does Surveillance monitor court registries and present that information as a basis for suspension, without serving the Company with the actual petitions?

CQ-5. Why did Surveillance classify the suspension as “Technical or Administrative” in the ESMA notification, but justify it as bankruptcy-based to the Company?

CQ-6. How many questions has Surveillance asked the former trustee about his disclosure practices during the 59-day bankruptcy?

CQ-7. Does Surveillance consider it proportionate to maintain a 37-day suspension against a confirmed victim of market abuse while sending that victim a 14-page questionnaire about one-day disclosure delays?

CQ-8. Is Surveillance aware that the continued suspension is actively preventing the Company from executing an institutional financing transaction that would protect 4,800 shareholders?

For the 4,800

I know some of you are reading this and feeling hopeless. You bought shares in a company that was supposed to build educational robots and expand into global markets. Instead, you got market abuse, a bankruptcy that should never have existed, a trustee who published nothing, a stock exchange that asks the victim 18 questions and the perpetrator zero, and a CEO writing 47-page responses from a personal laptop in Bucharest.

I understand the frustration. I share it.

But I want you to understand something: every single thing I have claimed has turned out to be true.

I said the bankruptcy was illegal. The High Court agreed — unanimously. I said there was market abuse. The regulator agreed — formally. I said the trustee violated MAR. The criminal complaint is open. I said the former board was negligent. The D&O claim is filed. I said Nasdaq’s suspension was unjustified. The DFSA has my complaint.

The EGM is Monday. New board. New auditor. 100 million shares authorized. Phase Education A/S.

We are four days away from a fully compliant, fully governed, fully operational listed company.

And all I am asking Nasdaq is one simple question: what do you need from us to let our shareholders trade?

Ask the AI

Have questions about any of this? The WildCEO AI agent has been trained on the full case archive — company announcements, court filings, Substack episodes, financial documents, the Nasdaq correspondence. Ask it anything.

The documents

The full 47-page response is available below

Shape Robotics response to Nasdaq, 10 April 2026 — 47 pages, signed, copied to Finanstilsynet

Nasdaq Surveillance letter, 10 April 2026 — 14 pages, unsigned, marked “Internal Use”

Finanstilsynet reprimand, 7 April 2026 — finanstilsynet.dk

Company Announcement No. 10-26 — Cision

EGM Agenda — 14 April 2026 — phase.education/egm

WildCEO AI Agent — wildceo.live

Previous episodes — substack.wildceo.live

GAME OVER | Day 37 — Subscribe at substack.wildceo.live for real-time updates as this case unfolds.

Shape Robotics A/S | CVR DK38322656 | Nasdaq: SHAPE | ISIN: DK0061273125

Mark-Robert Abraham, CEO — Vesterbrogade 74, 1620 Copenhagen V, Denmark